How To Calculate A House Payment: A Comprehensive Guide

Calculating a house payment is crucial for anyone looking to buy a home. Understanding how to accurately compute your monthly mortgage payment can save you a significant amount of money over time and help you manage your finances better. In this article, we will explore the essential components involved in calculating a house payment, including principal, interest, taxes, and insurance. Whether you are a first-time homebuyer or looking to refinance, knowing how to calculate your monthly payment can empower you to make informed decisions.

Additionally, we will break down the different types of loans available, how interest rates affect your payment, and provide practical examples to illustrate the calculations. By the end of this article, you will be equipped with the knowledge needed to confidently navigate the process of home financing.

Understanding your house payment is not just about knowing the numbers; it’s about making sure that you are financially prepared for this significant investment. Let’s delve into the details of calculating a house payment and explore the various factors that influence it.

Table of Contents

- Understanding the Components of a House Payment

- The Formula to Calculate Your Monthly Payment

- Types of Mortgages and Their Impact

- How Interest Rates Affect Your Payment

- Example Calculation of a House Payment

- Additional Costs to Consider

- Using Online Calculators for Quick Estimates

- Final Thoughts on Your House Payment

Understanding the Components of a House Payment

When calculating a house payment, it is essential to understand the four primary components involved:

- Principal: This is the amount of money you borrow to buy your home.

- Interest: This is the cost of borrowing money, expressed as a percentage.

- Property Taxes: These are taxes levied by your local government based on the value of your property.

- Homeowners Insurance: This insurance protects your home and belongings from damages and liabilities.

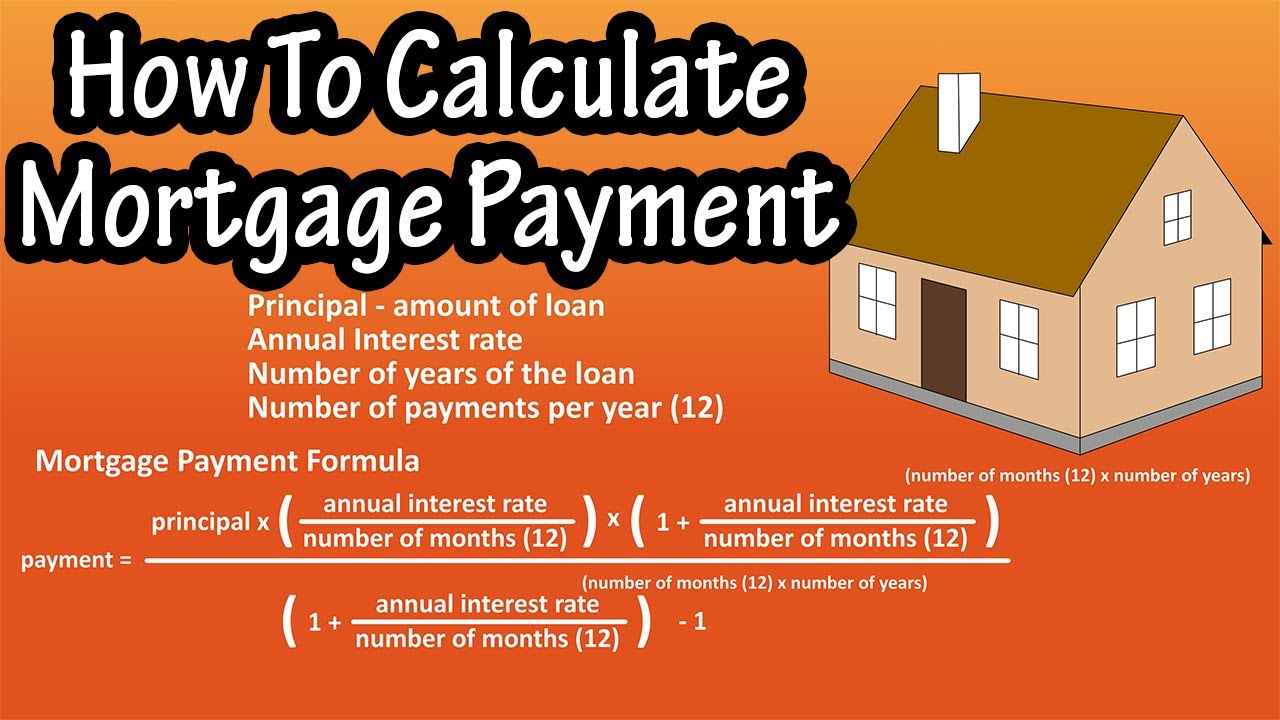

The Formula to Calculate Your Monthly Payment

The formula to calculate your monthly house payment (P) is as follows:

P = [r * PV] / [1 - (1 + r)^-n]

Where:

- P: Monthly payment

- r: Monthly interest rate (annual rate / 12)

- PV: Present value or loan amount

- n: Total number of payments (loan term in months)

Types of Mortgages and Their Impact

There are several types of mortgages, and each can affect your monthly payment differently:

- Fixed-Rate Mortgage: The interest rate remains the same throughout the loan term, providing stable monthly payments.

- Adjustable-Rate Mortgage (ARM): The interest rate may change after an initial fixed period, which can lead to fluctuating monthly payments.

- Interest-Only Mortgage: For a specified period, you only pay the interest, resulting in lower initial payments.

How Interest Rates Affect Your Payment

Interest rates play a pivotal role in determining your house payment. A higher interest rate means higher monthly payments, while a lower rate can save you money. For example:

- A $300,000 mortgage at 4% interest results in a monthly payment of approximately $1,432.

- At 5% interest, the same mortgage would result in a monthly payment of about $1,610.

Example Calculation of a House Payment

Let’s walk through an example calculation:

If you are purchasing a home for $350,000 with a 30-year fixed mortgage at a 4% interest rate, your calculation would look like this:

- Loan amount (PV): $350,000

- Annual interest rate: 4% (monthly interest rate = 0.33%)

- Loan term: 30 years (360 months)

Using the formula provided earlier, your monthly payment would be approximately $1,670. This includes only principal and interest; you would need to add taxes and insurance for the total monthly payment.

Additional Costs to Consider

In addition to principal and interest, other costs can affect your total monthly payment:

- Property Taxes: Typically, these are included in your monthly payment and can vary widely by location.

- Homeowners Insurance: The cost varies based on coverage and location.

- Private Mortgage Insurance (PMI): Required if your down payment is less than 20%.

Using Online Calculators for Quick Estimates

Online mortgage calculators can provide a quick estimate of your monthly payment without needing to perform complex calculations manually. These tools often allow you to input various factors, such as loan amount, interest rate, and loan term, to quickly see an estimate of your potential payment.

Final Thoughts on Your House Payment

Understanding how to calculate a house payment is an essential skill for any potential homeowner. By grasping the components that make up your monthly mortgage payment and how they interact, you can better prepare yourself for the financial commitment of owning a home. Always consider consulting with a financial advisor or mortgage professional for personalized advice tailored to your specific situation.

In conclusion, we hope this comprehensive guide has provided you with valuable insights into calculating a house payment effectively. If you have any further questions or would like to share your own experiences, please leave a comment below. Don’t forget to share this article with others who may find it helpful, and explore our site for more resources on home financing.

Thank you for reading, and we look forward to seeing you again soon!

Lowe's Company Stock Price: An In-Depth Analysis

Exploring The Allure Of Sexy Films: A Comprehensive Guide

If You Were The Last: A Journey Through Love, Survival, And Humanity

{kind=link}